Bildnachweis: ChatGPT.

Many European biotech companies still view the U.S. market primarily as a future exit channel. Yet it can be leveraged much earlier – not for selling, but for scaling up. This is precisely what is giving rise to a model that is becoming increasingly relevant for European biotech companies: the “biotech IP flip.” By Thomas Loeser

For a growing number of European biotech companies, the perspective on the role of the U.S. biotech ecosystem is currently shifting: The U.S. market is no longer viewed exclusively as a later exit channel but is increasingly being integrated earlier into their own scaling strategy. This is because the true strength of the U.S. ecosystem today lies not solely in the available capital. Rather, the decisive factor is the close integration of financing, clinical development, strategic pharmaceutical partners, specialized investment banks, their research teams, and institutional investors. It is precisely at this intersection that a model is currently emerging that is increasingly becoming of strategic importance for European biotech companies: the “Biotech IP Flip.”

Europe Lacks the Infrastructure for Scaling Up

The issue is not a lack of scientific excellence. Germany and Europe remain among the world leaders in biotechnology. Basic research is well-funded through grant programs and tax incentives and continuously produces technology platforms, datasets, and patents. However, the economic value is often generated elsewhere. Examples such as Gilead Sciences’ acquisition of Tubulis illustrate this dynamic perfectly. Only a relatively small group of European biotech companies manages to access the financing volumes required for product- and profit-oriented further development via NASDAQ IPOs or SPAC structures. In contrast, there is a large and growing number of early-stage projects that must continue to meet their capital needs through traditional VC financing in Germany and Europe. The real shortfall is often not the quality of science, but the lack of scaling infrastructure for building internationally competitive biotech companies.

Capital alone is not enough

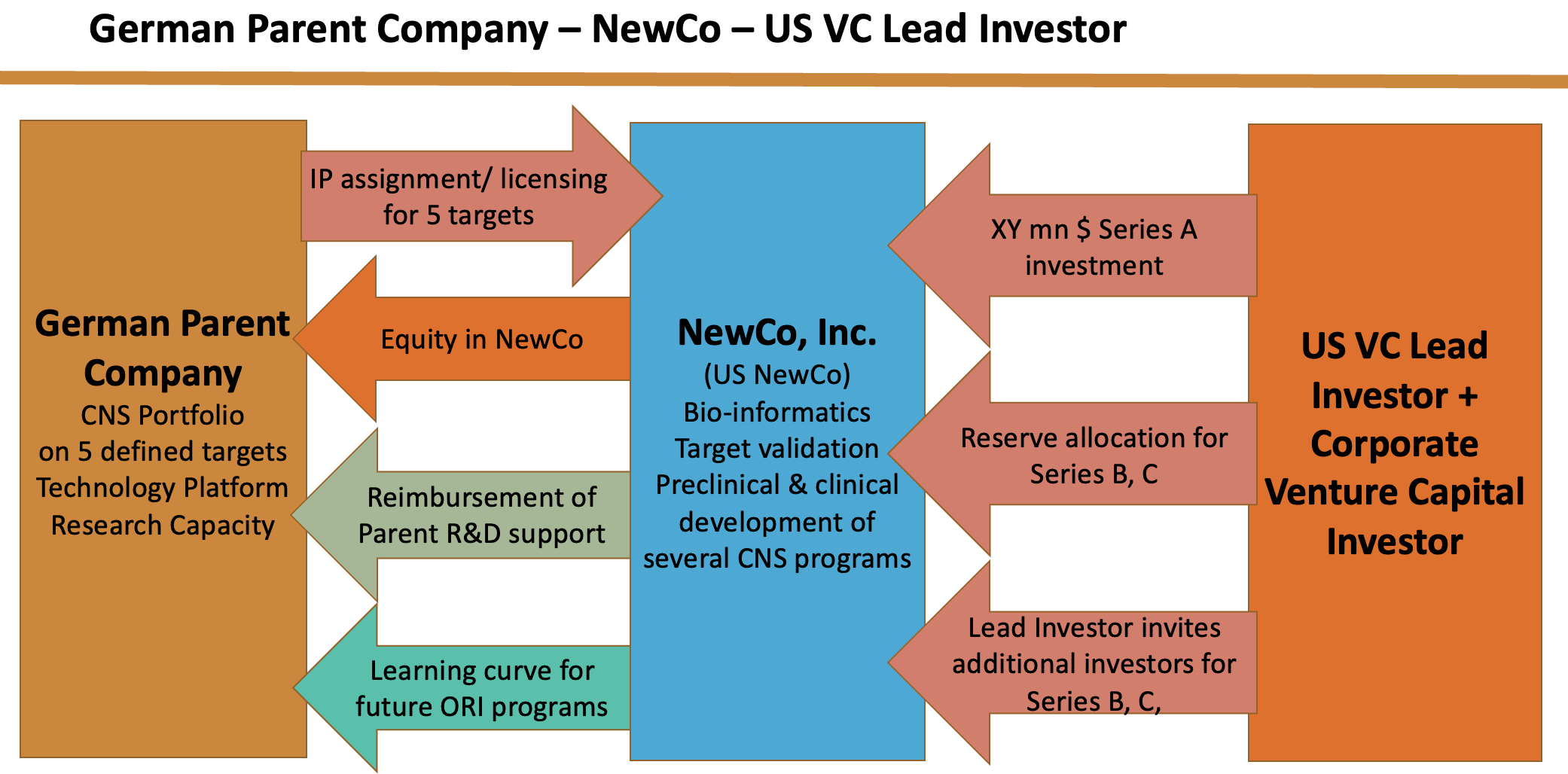

It is precisely this “funding dilemma” that has given rise to a model that combines financing, licensing, IP commercialization, and company building: the “Biotech IP Flip.” The concept is based on the structure of an “Equity-Based Licensing Deal” (EBLD) and has already been implemented several times by companies in the DACH region. Especially in the current market environment, this approach represents an attractive alternative to traditional fundraising models for many biotech companies.

- In a first step, the European IP parent company establishes a U.S.-domiciled subsidiary (“NewCo”) and equips it with the necessary development licenses. This not only preserves the underlying patent and IP structure of the European parent company. At the same time, cross-border commercial validation of European/German IP takes place within the U.S. market.

- In the second step, U.S. capital not only finances the further development of the assets. Multi-year research and development collaborations create additional revenue potential, operational partnerships, and new jobs on both sides of the Atlantic.

- The real strategic leverage, however, is unlocked by the third step: the US NewCo gains access to the U.S. life sciences ecosystem—to strategic pharmaceutical partners, specialized investment banks, their research teams, and institutional investors.

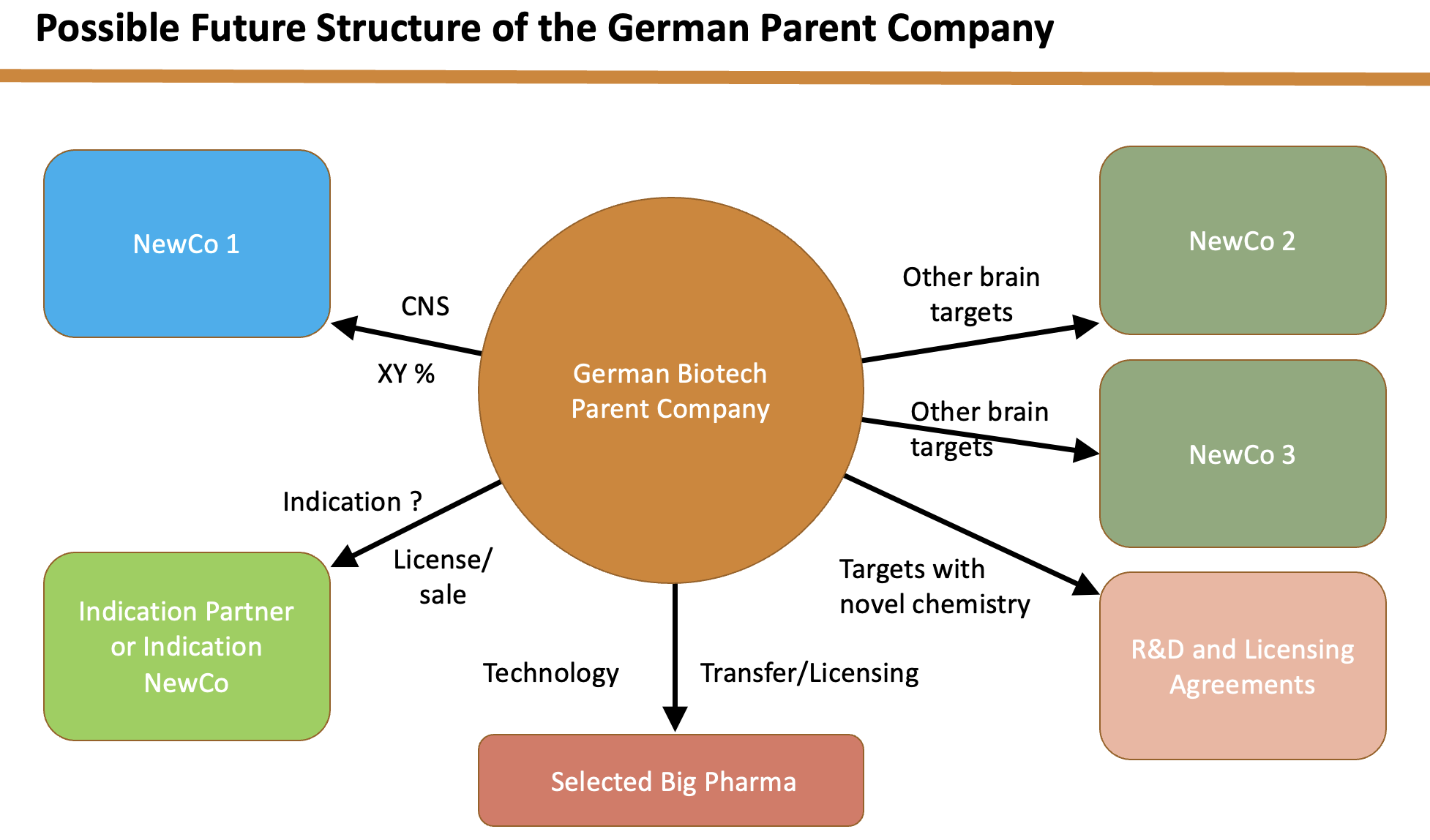

Establishing these strategic alliances and networks at an early stage opens up the option of either a future NASDAQ IPO as a stand-alone entity or positioning selected assets, programs or the entire company as a potential acquisition target for Big Pharma. Furthermore, this structure simultaneously supports the organizational and operational development of biotech companies capable of scaling internationally. The strategic scope for action now extends well beyond traditional IPO or trade sale scenarios—for example, toward secondaries, reverse mergers, or SPAC structures. In that sense, the biotech IP flip is less a financing instrument rather than an attractive model for upscaling.

Valuations in the billions rarely arise in isolation

Valuations in the billions rarely arise in isolation

The example of Numab AG and its wholly-owned U.S. subsidiary Yellow Jersey Therapeutics illustrates just how effectively this structure can work. In July 2024, Johnson & Johnson announced the acquisition of the company for approximately $ 1.25 billion. At the heart of the transaction was NM26, a novel bispecific antibody for the treatment of atopic dermatitis. What is remarkable here is not so much the sheer size of the transaction as its structure: Johnson & Johnson secured the global rights to a development program that was originally established within a European biotech environment but achieved its strategic scaling within a U.S. structure. According to Numab, NM26 targets IL-4 receptors as well as IL-31 and has the potential for a “first-in-class” treatment for atopic dermatitis. Johnson & Johnson also highlighted potential advantages over existing therapies and the upcoming transition to Phase 2 development. This is precisely where the strategic logic of the IP flip model unfolds its full potential.

The Journey from Martinsried to San Francisco

As early as 2018, Origenis GmbH – then based at the Innovation and StartUp Center for Biotechnology (IZB) in Martinsried – was pursuing a similar strategy to further develop its preclinical assets in the fields of ophthalmology and neurodegenerative diseases. While interest in the technology platform quickly materialized into a revenue-generating R&D collaboration with Expansion Therapeutics during a U.S. roadshow, the search for a partner to develop various therapeutic franchises proved to be significantly more complex. Consequently, Origenis’ management specifically sought a strategic investor for the neurodegenerative diseases franchise. This investor was ultimately found in Adam Knight, then a technology scout at Kleiner Perkins, who contacted Origenis management while searching for innovative targets and therapeutic approaches. The complementary positioning of Origenis as a drug discovery specialist with a proprietary and patent-protected technology platform and Kleiner Perkins as a partner and investor for the product-oriented and capital-intensive development of preclinical candidates through clinical development ultimately led to the implementation of the same three-stage structure.

With the founding of Neuron23 in San Francisco in 2018, a U.S. NewCo was established to which extensive licenses for proprietary small-molecule families were transferred for the development of candidates for neurodegenerative diseases using innovative mechanisms of action. In return, Origenis received an equity stake in Neuron23. Concurrently, an agreement was reached with Kleiner Perkins as anchor investor to implement the “IP prosecution strategy” in phases and to complete preclinical data sets based on defined milestones. After achieving these milestones, Neuron23 exited “stealth mode” in 2020 and closed a financing round of $ 113.5 million—with participation from additional investors such as WestLake Village BioPartners, Redmile Group, Cowen Healthcare Investments, HBM Partners and Acorn BioVentures.

With the founding of Neuron23 in San Francisco in 2018, a U.S. NewCo was established to which extensive licenses for proprietary small-molecule families were transferred for the development of candidates for neurodegenerative diseases using innovative mechanisms of action. In return, Origenis received an equity stake in Neuron23. Concurrently, an agreement was reached with Kleiner Perkins as anchor investor to implement the “IP prosecution strategy” in phases and to complete preclinical data sets based on defined milestones. After achieving these milestones, Neuron23 exited “stealth mode” in 2020 and closed a financing round of $ 113.5 million—with participation from additional investors such as WestLake Village BioPartners, Redmile Group, Cowen Healthcare Investments, HBM Partners and Acorn BioVentures.

To date, Neuron23 has raised a total of approximately $ 310 million across four funding rounds. The investor consortium now includes not only traditional U.S. blue-chip VCs but also crossover funds such as Perceptive Advisors and AI-focused investors such as the SoftBank Vision Fund. In particular, Neuron23’s AI-driven approach to developing “precision medicines for genetically defined neurological and immunological diseases” gives the company a unique positioning among potential NASDAQ IPO candidates—with corresponding value appreciation potential for the German parent company through its equity stake as well.

Complex – but increasingly relevant from a strategic perspective

The primary source of complexity in this model is concealed in its tax and structural implementation – particularly at the level of the European parent company holding the patent. First, IP-related issues must be addressed through an “IP Assignment and License Agreement” as well as supplementary “Master Service Agreements” for further research and development work. At the same time, a long-term “IP Prosecution Strategy” is typically defined in collaboration with the investor syndicate.

In parallel, three tax issues in particular require heightened attention:

- the confirmation of a tax-optimized model at the corporate and individual shareholder levels,

- the avoidance of double taxation or the taxation of “paper profits,”

- as well as the consideration of potential issues such as hidden profit distributions or the realization of hidden reserves.

However, by involving specialized tax firms and auditors at an early stage and, where necessary, obtaining binding rulings from the tax authorities, these issues can now be addressed in a structured manner.

Timing becomes a strategic decision

Timing becomes a strategic decision

The Biotech IP Flip is thus far more than just an alternative financing structure. The model combines European scientific excellence with U.S. growth capital, strategic networks, and the scaling opportunities of the U.S. biotech ecosystem—without necessarily having to completely abandon the technological foundation. Especially in a capital market environment increasingly shaped by AI, platform, and infrastructure logic, international scaling structures are gaining additional importance. Accordingly, capital is becoming more selective, and investors are increasingly prioritizing platform, AI, and precision medicine approaches. As a consequence, early strategic access to the U.S. ecosystem could become a decisive competitive factor for European biotech companies. In the future, what matters may no longer be solely where innovation originates, but rather where the upscaling is going to take place.

Autor/Autorin

Thomas Loeser

Thomas Loeser is a Senior Advisor to IP Lab Ventures Fund I, Prague/CZ, and has more than 3 decades of international experience as a CFO of European and U.S. biotechnology companies. With a focus on transatlantic company building, strategic financing, and U.S. capital markets, his areas of expertise include fundraising, M&A, IPOs, in- /out-licensing deals, and the commercialization of IP portfolios. In his CFO role at Origenis GmbH / IZB Martinsried, he promoted the establishment of Neuron23, Inc. in the U.S., which has raised approximately $ 310 million since 2019 from investors such as Kleiner Perkins and the SoftBank Vision Fund 2. Prior to that, he led the financing strategy at ESBATech AG in Zurich, whose pre-clinical ophthalmology franchise was sold to Alcon in 2009 for up to $ 589 million. Thomas Loeser studied business administration at Ludwig Maximilian University of Munich, where he served as an assistant lecturer, and completed the Advanced Management Program at Harvard Business School (AMP 166). He has been a member of the Harvard Alumni Association since 2004.